A ‘Big Short’ Investor’s New Bet: Climate Change Will Bust the Housing Market

Credit to Author: Geoff Dembicki| Date: Fri, 01 Nov 2019 13:25:57 +0000

In 2007, almost no one would admit what became obvious in hindsight: The housing market was on the brink of collapse and would take a good chunk of the U.S. economy along with it. Lenders were getting rich, giving home loans to people who couldn’t afford them, investment banks were making a killing by combining those shaky loans into securities, ratings agencies cashed in by certifying those securities as safe and millions of ordinary people got screwed when the whole thing came crashing down.

But David Burt saw it coming. The investor was a consultant at Cornwall Capital, the firm that shorted the subprime mortgage market and made $80 million as some of Wall Street’s biggest firms imploded around it. It was such a spectacular, farsighted bet against the conventional wisdom surrounding the housing market boom that Cornwall was profiled in Michael Lewis's book The Big Short, and one of Burt's colleagues was played by Brad Pitt in the movie adaptation. The thing, though, is that many of the risk factors leading up to the crash were fairly easy to spot if you weren’t earning massive profits dependent on ignoring them.

“There’s some really big incentives problems in markets,” Burt explained recently at a hotel café on New York’s Upper East Side. “Whether it’s conscious or subconscious, and it’s not necessarily nefarious, a lot of the time it’s just easier for people to do the thing that’s best for them in some easy-to-conceive-of timeframe.”

Now Burt thinks there could be another financial disaster growing inside the real estate market. But this time, the bubble is being inflated by climate change denial.

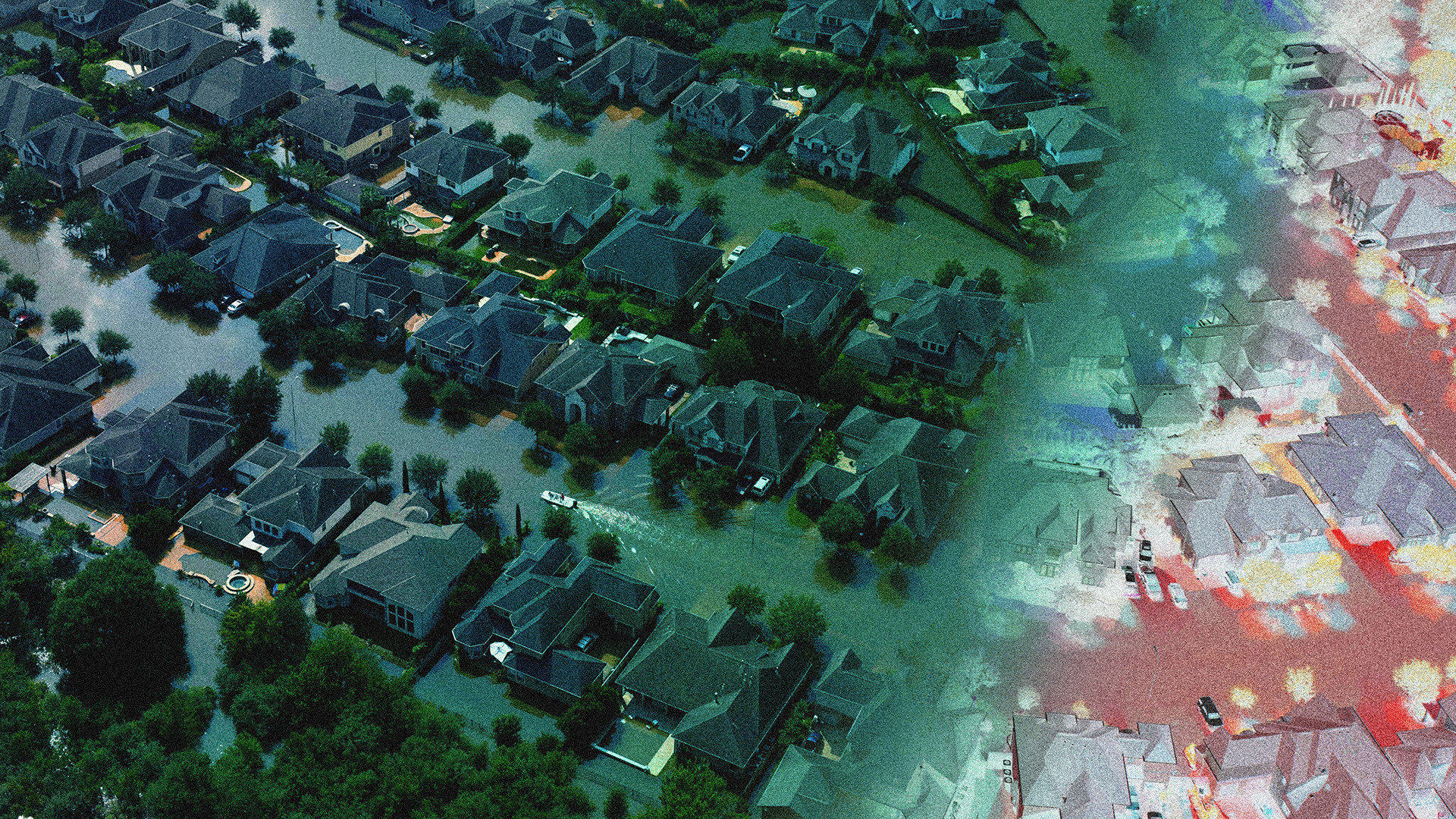

We tend to conceive of global temperature rise as a slow, steady and predictable threat: humans release emissions, the atmosphere gets warmer and sea levels get higher and higher. But the disaster Burt thinks the markets are ignoring could strike a lot sooner and more abruptly. It would likely be felt first in Texas, Florida, New Jersey, California or anywhere else with a ton of homes and other real estate exposed to flooding, and then spiral outwards into the financial system, potentially wreaking destruction rivaling what happened in 2008.

To understand the mechanics of this threat it helps to visualize the market for coastal real estate as a brand new condo tower on the beach. The foundations for this tower are built upon maps drawn by the federal government that seriously downplay the likelihood of sea-level rise and floods. The lower floors are filled with homeowners paying off mortgages on homes that could be chronically flooded within the next few decades. The penthouse is occupied by banks and other investors turning those mortgages into ever more complex investments. Though it’s hard to predict a specific event that knocks this tower to the ground—perhaps it could be a devastating $1 trillion Florida hurricane, or a stampede to the exits by investors once denial of climate dangers turns to fear—it’s clear to anyone paying attention that the entire structure is teetering in the ocean wind.

Burt sees similarities between now and the lead-up to 2008. “There’s a lot of parallels, it’s a big real estate mispricing issue. At its core that presents a lot of the same risks. A lot of real estate is massively overpriced and there’s a lot of risk associated with that and the big risk is another foreclosure crisis,” he said. “Now, it’s a very different dynamic that’s creating the mispricing but actually magnitude-wise it looks pretty similar, maybe even bigger.”

Like he did before the last crash, Burt has left his full-time investing job, this time at the $1 trillion Wellington Management. He now heads an investment firm which is focussed on financial opportunities in a real estate market threatened by climate change, some of which could materialize as early as next year. This places him in a similarly complex moral position—a plunge in housing values due to the market either collapsing or else accurately pricing the true risk of flooding might be terrible for millions of people, but also creates the chance for smart investors to earn a lot of money. Just as Cornwall cashed in while people lost their homes, Burt could profit in the aftermath of a devastating financial storm.

Though this is far from a mainstream perspective on Wall Street, he’s not the only prominent insider warning of the gigantic financial risks of climate change. “There will be ongoing, massive events, weather events, taking place, exposing potentially trillions of dollars of real estate to coastal flooding and damages,” Ed Delgado, a former executive at the mortgage entity Freddie Mac, told CNBC earlier this year.

Yet the market is acting as if climate change doesn’t exist. Anywhere between $60 billion to $100 billion worth of mortgages for coastal homes are issued each year. “We’re continuing to build in these flood hazard zones,” said Matthew Eby, founder and executive director of the First Street Foundation, a non-profit research group that studies flood risk. “You end up with a very scary looking situation.”

In the years leading up to the 2008 crisis, Burt worked at the investment giant BlackRock, where his job was to identify subprime mortgage bonds that were likely to go bad. He soon came to the realization that the entire subprime market was way more fragile than anyone wanted to admit. “Some of it was kind of obvious. It was pretty clear that the loans getting made probably shouldn’t be made,” he said. “People were making so much money as the market expanded that just entertaining this somewhat obvious downside risk proposed a big risk to their livelihood.”

Burt left BlackRock to bet against the subprime housing market on his own and through his lawyer was introduced to Charlie Ledley and Jamie Mai of Cornwall Capital, two Wall Street outsiders from California who also saw the potential for collapse. They paid Burt $50,000 a month to run and analyze data models predicting how various house price scenarios could vaporize investments that most of the financial world considered unassailable.

Burt also brought valuable connections to Cornwall. At a 2007 subprime convention in Las Vegas—where Ledley at one point shot Uzis and Berettas at a firing range with salespeople from the investment bank Bear Stearns—Burt set up meetings with Wall Street insiders that allowed Cornwall to make large financial bets on the market failing. A year later, Bear Stearns had collapsed, the global economy was entering freefall and everyone at Cornwall, in addition to other investors featured in The Big Short, looked like geniuses.

“Burt in turn has placed much of the blame for what Wall Street did on perverted incentive compensation schemes which enabled so-called experts to create pools of mortgages, to be sold to an unsuspecting public, on the basis not of the quality of the bonds but of the amount of bonds they could sell,” an investor and colleague of Burt’s named David Scudder later explained.

At every stage of this process people were blinded to the dangers of what they were doing by their own self-interest. Now, as before, perverted incentives around climate change are amplifying risk in the housing market—and, potentially, the wider financial system.

Let’s return to that image of the market as a coastal condo tower. At the tower’s foundation, right where concrete rises from the sand, you have the flood maps created by the Federal Emergency Management Agency (FEMA). These flood maps are so important to the market because they help determine the financial risk that any given home or property will be flooded. If the risk of flooding is high, then a homeowner pays a larger premium for the flood insurance he or she buys from the federal government’s National Flood Insurance Program.

In theory this should help provide a stable foundation to the real estate market, because people will be less likely to build, buy or sell homes in high-risk flood areas, or else pay a higher price for doing so. But that only works if the flood maps are accurate, and research from First Street Foundation suggests that 75 percent of FEMA’s flood maps are out of date; some of them haven’t been revised since the 1970s. Even the most current maps might be doing a poor job of showing how exposed homes and other buildings are to flooding and weather disasters.

“The maps are made looking at historical observations,” Eby said. And basing future flood predictions on what’s happened in the past “doesn’t make sense from our perspective,” he went on, because greenhouse gas emissions, ocean temperatures, sea levels and other risk factors for catastrophic flooding are at record highs and show no signs of plateauing. There is literally no precedent for the dangers hurtling towards us.

Now let’s look at the lower floors on our imagined condo tower. Relying on flood maps that are out of date or incomplete, people are buying homes without knowing the true risk of their investment. They could be purchasing one of the 311,000 coastal homes that the Union of Concerned Scientists calculates will be chronically flooded within the next 30 years, meaning those properties are at risk of becoming worthless before their mortgages are even paid off. This is a risk that rises significantly along the coasts of California, Texas, Louisiana, Florida, South Carolina, North Carolina, Maryland, New Jersey, and New York.

These lower floors of the market are also filled with people who already own homes that have a high likelihood of flooding, but aren’t located in a FEMA-designated flood zone. This artificially inflates the value of their homes because they don’t need to pay for flood insurance. But it also means that when a disaster strikes there is no insurance to cover the damages. That’s what happened to 80 percent of the Houston homes flooded by Hurricane Harvey in 2017 and the impacts were nearly catastrophic. “Houston could have seen a massive foreclosure crisis were it not for strong investor demand in the market,” CNBC reported.

Now we come to the penthouse. This is the part of the market where individual mortgages for homes, many of which are at risk of going literally underwater, get traded around by banks and other Wall Street players. Researchers from John Hopkins University and HEC Montreal earlier this fall found that banks are selling potentially risky mortgages to the government-backed entities Freddie Mac and Fannie Mae. This is a good deal for the banks, because regulations prevent Freddie Mac and Fannie Mae from factoring the growing risk of natural disasters into the prices that they pay.

So, banks get to profit from all the floors of the figurative condo tower below them, while offloading many of the financial risks to entities—Freddie Mac and Fannie Mae—that are funded by taxpayers. This might increase the incentive to keep making home loans in risky and vulnerable areas. The danger is that if the lower floors start imploding because of a horrific natural disaster or flooding that jacks up the price of insurance to levels unaffordable to homeowners, causing a foreclosure crisis, then the entire tower could collapse.

“The findings echo the subprime lending crisis of 2008, when unexpected drops in home values cascaded through the economy and triggered recession,” the New York Times wrote of the report from John Hopkins University and HEC Montreal. “One difference this time is that those values would be less likely to rebound, because many of the homes literally would be underwater.”

In such a scenario, Burt and those who invested with his fund would make money. But he insists that that's not his sole motivation. He wants people to wake up and realize what he has, that the housing market—along with so many other things—could be wrecked by climate change.

“I love the environment and nature and much of my joy in life comes from going for walks in the woods or on the beach with my family,” he said. “We have no idea how bad things really could get, there’s far bigger risks associated with climate change than depreciating home values and some of them are just really, really scary.”

Burt glanced at the time and realized he had to leave. He had investors to meet.

Sign up for our newsletter to get the best of VICE delivered to your inbox daily.

Geoff Dembicki is the author of Are We Screwed? How a New Generation Is Fighting to Survive Climate Change. Follow him on Twitter.

This article originally appeared on VICE US.